As we enter the final month of 2020, we reflect on the rapid changes the legal market has endured, starting with a look at the last "normal" quarter, Q1

As we round into the final month of 2020, taking a moment to reflect on the rapid changes the world and the legal market have endured can be a quite useful refresher on how we have gotten to this point.

No one could have predicted the dramatic changes the legal market and world at large would have undergone as a result of a global pandemic leading into 2020. The wholesale deviations from the “norm” that rapidly occurred somewhat decreased the value of the 2020 Report on the State of the Legal Market as 2019 financial performance couldn’t accurately be used as a guide of what is to come.

At the same time, the COVID-19 pandemic served as a catalyst for change, accelerating the industry from a tepid pace of incremental change that typified the market for many years to a period of radical change, a main message of the report. This included, but was not limited to, a seemingly overnight shift to work-from-home for a substantial proportion of practicing lawyers in the country by the end of Q1 2020. Indeed, this was something that was not thought to be possible pre-2020 because it was supposed that lawyers working remotely would be a drag on productivity and thus profitability. As these assumptions have been challenged, perhaps this change will prove contagious, providing an opportunity for law firms to continue to reimagine the delivery of legal services going forward.

I want to look back at the last quarter that we can truly call the “old” normal — Q1 2020. This review can provide a potential preview to what the legal market might return to in a vaccinated world, or what might be a peak in performance for the foreseeable future.

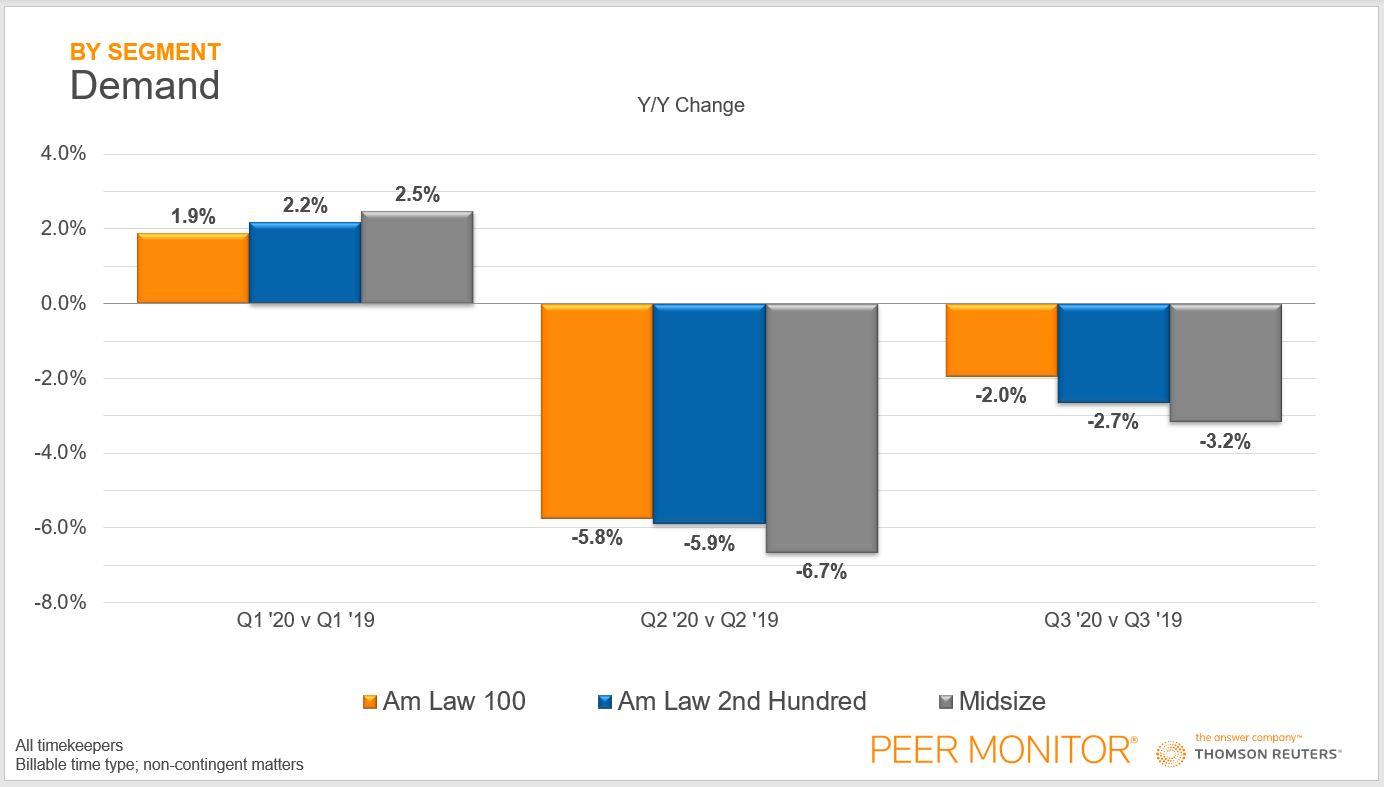

Pandemic’s impact on legal demand

To start our review of Q1 2020, we will begin with demand, or average billable hours worked per firm. This increased by an impressive 2.0% on average in the first quarter, which represents demand’s strongest first quarter performance in roughly a decade. This came on the heels of 2018 and 2019 which both marked the first time the legal market had consecutive years of positive demand growth since the end of the Great Recession. Couple this with near all-time highs in lawyer growth during this same period, and it appeared that firms were prepared for a period of continued growth, with Q1 2020 reflecting great optimism in the legal industry.

That market strength and optimism is partly due to the fact that midsize law firms outside the Am Law 200, which have lagged their larger counterparts for most of the last decade in terms of demand, became market leaders in average demand growth during the first quarter, a feat that had not occurred since 2016.

As the world collectively sheltered during the second quarter, legal demand was sure to deflate. While all firms saw significant contractions in legal demand above 5.0%, midsize law firms saw the worst performance of the three segments, maybe in part because many of midsize firm clientele are also smaller and suffered greater financial damage at the onset of the pandemic lockdowns. The old adage “Firms only do as well as their clients do” comes to mind. Or perhaps this is simply a reflection of the resiliency of scale as our Am Law 100 firms have had the best relative performance during both of last two quarters of demand shortfalls.

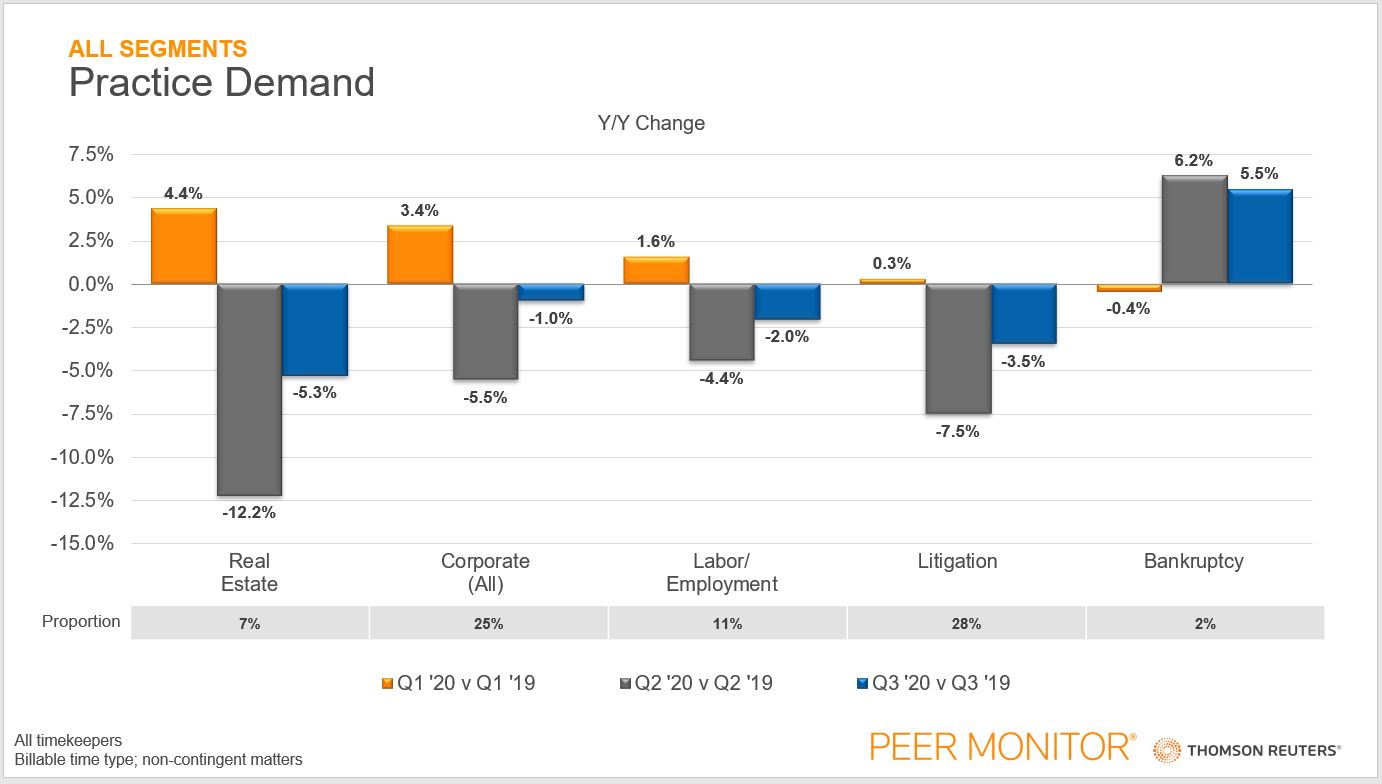

While midsize law firms went from drivers to laggards in demand, so did some notable practice areas.

Practice area contraction

Real estate, not only led all practice areas in Q1 demand growth, but also enjoyed the strongest quarterly growth for the practice in the history of Peer Monitor collected data. Then, within the next six months, the practice area records the two largest quarterly contractions in its history, seeing a mammoth 12.2% drop in Q2, and an alarming 5.3% contraction in Q3. With commercial real estate, especially in majority cities, becoming a clear loser in the broader U.S. economy due to the increased prevalence of working from home, this practice area is sure to encounter strong headwinds moving forward.

The Corporate and Labor/Employment practices also saw strong signs at the beginning of 2020 and have continued to show strong relative performance as compared with the market-wide demand contraction of 5.9% in Q2 and 2.4% in Q3. On the other side of the token, Litigation has lagged overall demand, which fell to an even greater extent once the world shut down in Q2, but also has continued to lag even when U.S. started reopening in Q3. Perhaps, the transition for courts to go virtual has not been as successful as some had hoped.

Bankruptcy, which saw nearly 10 years of quarterly contraction pre-2019, has put together two solid quarters of growth of 5.0% or greater. While it’s not surprising that bankruptcy contracted before the pandemic as the U.S. economy saw a decade of economic growth, it is also not surprising to see success in this area since the onset of the pandemic.

Hopefully, 2021 does not contain the drastic change that will no doubt be etched into 2020’s tombstone, but insane and unpredictable things do happen. As we’ve seen, areas or categories that are market leaders one quarter can be dragging down the same metric the next, which makes data-driven decision-making all the more important to make sure law firms avoid the kind of reversal of fortunes that 2020 wrought on all of us.