Law firms are increasingly using the idea of strategic innovation to fundamentally improve the delivery of legal services & provide better value to clients

This article was written by Edson Kawabata, the Chief Operating Officer at Machado Meyer, a leading law firm in Brazil.

By definition, strategic innovation is an enabler to a law firm’s success. It is not the means, like new software or other technological advancements; rather it is the way, the manner in which law firms advance.

This is true no matter how a firm measures its success — by profit growth, client preference, market reputation, or simply offering superior value to clients.

In many law firms, profit per partner is still the traditional yardstick of firm success, of course; though many firms are expanding their view. Strategic innovation, for example, is increasingly being used to fundamentally improve the delivery of superior value to clients. And this value itself is measured in terms of responsiveness to business, streamlined content, embedded expertise, work agility, as well as an open and trusting relationship. These key attributes (to name just a few) revert to better results by necessity.

But how do law firms get there? How do they create an environment in which strategic innovation, not a focus on immediate profit, is the driver of all things?

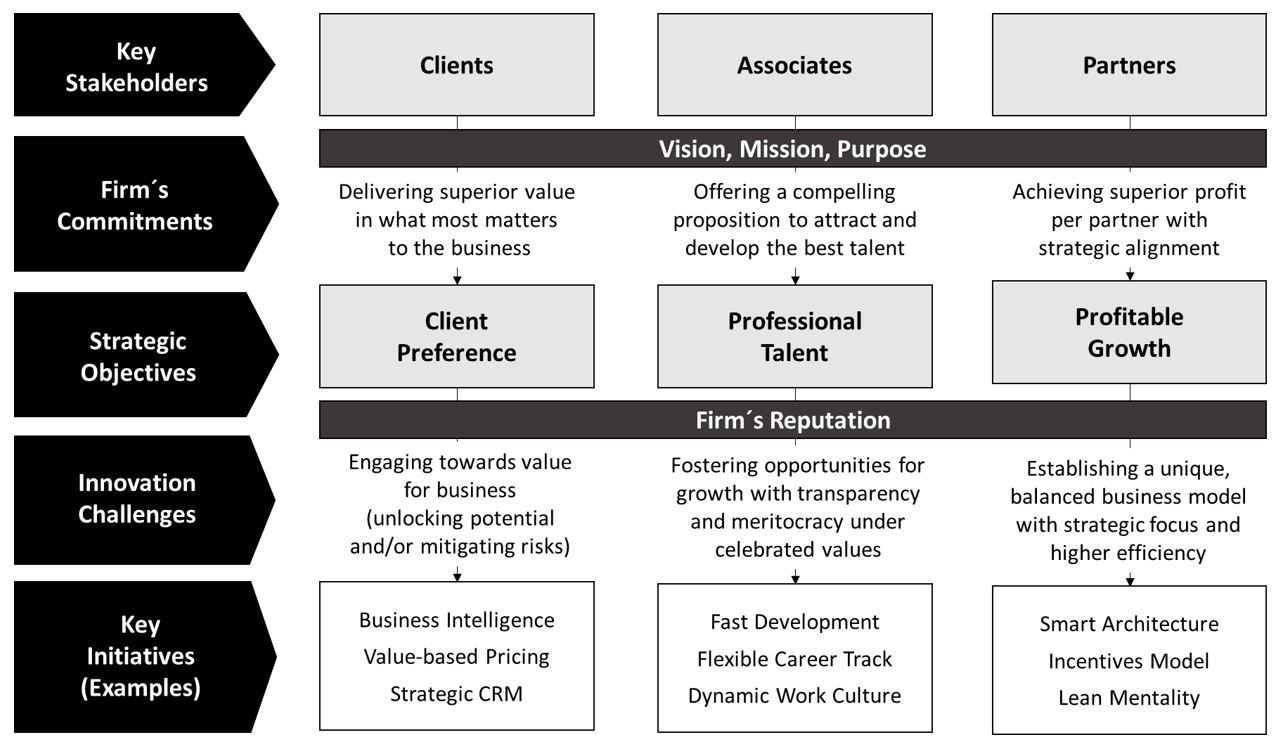

I would argue that to do this, it is important from the beginning to strike the right balance of goals across three main groups of stakeholders — clients, partners, and associates. I think that most firm leaders tend to take the partners’ point of view as the stacking point, and then consider the clients’ needs. Too often, in the middle, are the associates — those people that actually run most of the activities that make the delivery of legal services possible — and who are given little thought. So, this will be one of the key elements for law firms to achieve this balance across these three types of stakeholders — consider all as part of an integrated equation.

As we see in the chart below, each of these groups should have specific commitments, objectives, and challenges because basically each in their own way will be setting the strategic expectation for legal service delivery. Further, firms need to be looking ahead at what the role of innovation would be for each of these groups in order to best maximize delivery against these objectives.

The Drive Toward Strategic Innovation

Let’s start with the partners. Of course, the partners’ strategic objectives is to keep the firm on a path of profitable growth. And the law firm’s commitment to its partners and to that objective is to strategically align partners with the talent (associates) and resources (operational structure and technology) that allows partners to deliver on this goal. And, as the chart suggests, one key way to keep the firm on a path to profitability is for the partners to ingrain into the firm a business model that focuses on higher efficiency through more effective work process methods and leaner management.

And this links directly to the commitment that firms have to their clients. I’ve spoken to many clients, and while some clients simply choose the firms they like, many more select those firms that are dedicated to understanding the clients’ business and providing value where the client needs it most. And a big part of that is operating in a way that will ensure what the firm charges clients reflects the efficiencies and compensation models the firm has in place, with focus and objectivity.

Thus, as the firm tries to position itself in the eyes of the client as a select firm — or even better, as a trusted advisor — it becomes more crucial for the firm to focus on innovation in areas of client relationship management, business intelligence, and alternative pricing programs to demonstrate its value.

The final group of stakeholders — the firm’s associates — are a vital part of this balance, and not one to be overlooked. For a law firm to achieve success at any level, talent is needed; and talent is typically attracted by challenge, reputation, and compensation. Challenge is how the firm defines its mission, vision, or purpose. The best law firms position themselves as unique, genuine, and committed to building on their reputation — not just as a marketing piece, but as a truly inspiring place to work. And much of that inspiration comes from the firm’s drive to excel and innovate.

So, it is the balance of the firm’s commitments to these three stakeholders — the partners, the associates, and the clients — that will be essential to the firm’s overall success.

As the chart shows, talent and resources circulate through the life system of the law firm. The stronger the system, the more talent and resources it can put to use in pursuing innovation. That’s why firms need to continuously improve their business model in terms of efficiency and strategic innovation.

Is this model too simplistic? Perhaps… but maybe we should ask the doers. There are plenty of knowledge around as well as a lots of recipes; but nothing teaches like the real experience. Success in today’s legal industry demands talent, consistency, commitment, and a strong resilience — indeed, a push to succeed.

Of course, this is no big news to anyone in the industry. However, as The Matrix’s Morpheus said to Neo: “There’s a difference between knowing the path and walking the path.”

Increasingly, those law firms committed to strategic innovation as a way of continuously improving and keeping their firm in balance among partners, associates, and clients are those that are much more likely to reach the next level among their competitors and peers.